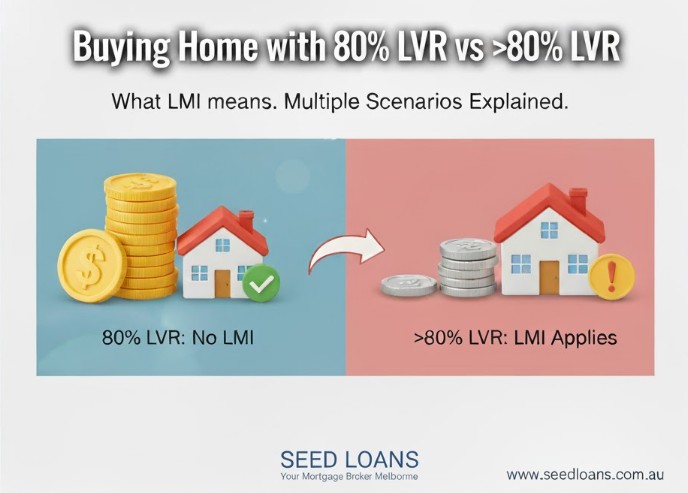

For many first home buyers in Glen Waverley, Melbourne, the dream of owning a home is closer than they think. However, the world of mortgages can feel like a complex process, filled with confusing terms like LVR and LMI.

At SEED LOANS, your dedicated Mortgage Broker team, we believe in making the home loan application process clear, simple, and stress-free. Understanding two key concepts—Loan-to-Value Ratio (LVR) and Lenders’ Mortgage Insurance (LMI)—is essential for securing the best home loan for your financial future.

This guide will break down what these terms mean, compare the pros and cons of an 80% LVR versus a higher LVR, and show you how we can help you navigate these choices.